The world of corporate Bitcoin adoption has entered a bold new chapter. Michael Saylor, the Chief Executive Officer of Strategy (formerly MicroStrategy), has unveiled a sophisticated financial framework that he believes will fundamentally redefine how corporations interact with Bitcoin as a treasury asset. At the heart of this framework is a 30% Bitcoin yield model — a structured approach to generating returns from Bitcoin holdings that Saylor publicly calls the future of digital credit. This announcement has sent ripples across the cryptocurrency industry, financial markets, and institutional investing circles alike.

For years, Saylor has been one of the most vocal advocates of a Bitcoin accumulation strategy in the corporate world. Strategy has acquired billions of dollars worth of Bitcoin on its balance sheet, pioneering the idea that companies can use BTC as a primary reserve asset rather than cash or bonds. His claim that this approach represents the future of digital credit markets is as ambitious as it is provocative.

This article breaks down exactly what Saylor’s 30% Bitcoin yield model entails, how it works, why it matters for institutional investors and corporate treasuries, and what it could mean for the broader trajectory of Bitcoin adoption in finance.

What Is the Strategy CEO’s 30% Bitcoin Yield Model?

The “yield” in this context is not a traditional interest payment but rather a Bitcoin-per-share accretion metric — a measure of how much Bitcoin each share of Strategy stock represents over time.

Saylor has framed this yield target of 30% annually as the rate at which Strategy aims to increase its BTC holdings per diluted share. When the model works as intended, shareholders benefit not just from any price appreciation in Bitcoin itself, but also from the growing amount of Bitcoin that backs each share they own.

Why Saylor Calls This the Future of Digital Credit

Saylor’s vision extends well beyond Strategy’s own balance sheet. He has articulated a broader argument that Bitcoin-backed credit markets will eventually become a foundational layer of the global financial system. In his view, Bitcoin’s properties — fixed supply, decentralization, censorship resistance, and global liquidity — make it the ideal form of sound money collateral for a new generation of lending and credit instruments.

Traditional credit markets rely on government bonds, real estate, or corporate cash flows as the underlying basis for lending. Saylor argues that these assets are inherently inflationary and subject to counterparty and sovereign risk. This, he contends, makes it uniquely suited to serve as the backbone of a parallel credit system — one that operates on the principles of sound monetary policy rather than central bank discretion.

How the 30% Yield Target Is Calculated and Tracked

Understanding the mechanics behind the 30% BTC yield target requires a closer look at how Strategy tracks and reports its Bitcoin performance. The company has introduced a proprietary metric called “BTC Yield,” which measures the percentage change in the ratio of Bitcoin holdings to diluted shares outstanding over a given period.

This approach is clever because it aligns management incentives with long-term Bitcoin accumulation rather than short-term earnings per share. It also provides a transparent, easy-to-understand benchmark that investors can track in real time. Critics, however, have noted that this metric can be gamed through aggressive equity dilution, and that the 30% target may prove difficult to sustain as Strategy’s Bitcoin holdings grow larger and the marginal cost of accumulation rises.

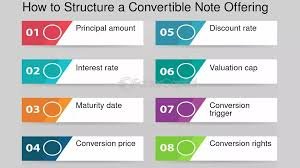

The Role of Convertible Notes and Equity Offerings in the Model

A central pillar of Strategy’s Bitcoin financing strategy is the use of convertible notes — a form of hybrid debt that can be converted into equity at a predetermined price. These instruments allow the company to raise large amounts of capital at relatively low interest rates because investors receive the option to participate in Bitcoin-driven equity upside.

Equity offerings serve a similar purpose. When Strategy’s stock trades at a significant premium to its net asset value in Bitcoin, the company can sell shares and use the proceeds to buy more Bitcoin — a process that is immediately accretive to the BTC-per-share ratio. This premium, often called the “MSTR premium,” has at times been substantial, giving Strategy a structural advantage in accumulating Bitcoin relative to simply holding it directly.

Institutional Implications and the Broader Bitcoin Treasury Trend

Strategy’s model has not gone unnoticed by other corporations. A growing number of companies have adopted some version of the Bitcoin treasury strategy, inspired by Saylor’s pioneering approach. From small-cap tech firms to publicly listed mining companies, the idea of holding Bitcoin as a primary reserve asset has gained significant traction in the post-2020 era of monetary debasement concerns.

The institutional implications of a widely adopted 30% Bitcoin yield framework are significant. If multiple large corporations begin competing to accumulate Bitcoin through debt and equity financing, the demand pressure on BTC supply could be considerable. Bitcoin’s hard cap of 21 million coins means that increased institutional demand has the potential to create sustained upward price pressure over time — a dynamic that Saylor has explicitly pointed to as part of the thesis behind his model.

Risks and Criticisms of the Model

No financial model is without risk, and Saylor’s 30% Bitcoin yield strategy has attracted its share of skepticism. The most fundamental concern is leverage. Strategy’s approach relies heavily on debt financing, which means that a prolonged decline in Bitcoin’s price could create significant stress on the company’s balance sheet. If BTC falls sharply, the collateral value supporting the debt decreases, potentially triggering margin calls or forcing asset sales at unfavorable prices.

There is also the question of sustainability of the 30% target. In the early stages of the model, when Strategy’s Bitcoin holdings were smaller and its stock commanded a high premium, executing accretive purchases was relatively straightforward. As the company’s Bitcoin position has grown to over half a million coins, the scale of transactions required to move the BTC Yield needle has increased dramatically. Some analysts question whether a 30% annual target remains achievable without taking on excessive risk.

What This Means for the Future of Bitcoin in Finance

Despite the risks, Saylor’s vision of Bitcoin as the foundation of digital credit represents a genuinely novel and thought-provoking framework for thinking about the intersection of cryptocurrency and traditional finance. The concept of Bitcoin yield — measured not in fiat interest payments but in BTC per share accretion — could eventually become a standard metric in investment analysis, just as earnings per share or dividend yield are today. Saylor’s work at Strategy is essentially a live experiment in building the financial infrastructure of a Bitcoin-native economy, conducted in full public view on one of the world’s most transparent markets.

Conclusion

Michael Saylor’s 30% Bitcoin yield model is more than a corporate financial strategy — it is a manifesto for the future of digital credit and Bitcoin-based finance. By reframing yield in Bitcoin terms, leveraging convertible notes and equity offerings to drive BTC accumulation, and positioning Bitcoin as the ultimate collateral for a new credit system, Saylor has outlined a vision that is equal parts revolutionary and controversial.

Whether or not Strategy achieves its ambitious 30% annual BTC yield target, the model has already succeeded in reshaping the conversation around institutional Bitcoin adoption. It has demonstrated that Bitcoin can be integrated into sophisticated corporate finance structures, that investors will accept Bitcoin-denominated performance metrics, and that there is real institutional appetite for Bitcoin-backed financial products.

Also More: Why Bitcoin is Up Today Market Analysis & Price Drivers 2025