Blockchain technology has quickly moved from a niche concept associated only with cryptocurrencies to a foundational digital infrastructure that many experts compare to the early days of the internet. At its core, blockchain technology promises something extremely valuable in the digital age: the ability to create trust without relying on a single central authority. Instead of one company, bank, or government maintaining the records, a blockchain distributes data across many computers in a transparent and secure way. This shift has opened the door to new business models, digital assets, and innovative applications that challenge long-standing systems in finance, supply chains, identity management, and more.

To understand why blockchain technology has become such an important topic, it helps to consider the problems it aims to solve. Traditional digital systems rely heavily on centralized databases, which can be vulnerable to hacking, manipulation, or simple human error. If a central database is compromised, every user connected to it can be affected. In contrast, blockchain technology uses a distributed ledger, where each transaction is recorded across a network of independent nodes. This makes it much harder to alter past data and creates a level of transparency that is difficult to achieve with conventional systems.

Another reason blockchain technology is receiving so much attention is its potential to remove intermediaries from many processes. Sending money internationally, clearing trades in financial markets, recording property rights, or verifying product authenticity usually requires multiple organizations to check, approve, and update records. These steps add cost, delay, and complexity. Through smart contracts and decentralized applications, blockchain technology can automate many of these tasks, reducing friction and enabling near real-time transactions that are recorded on an immutable ledger.

At the same time, blockchain technology is not a magic solution to every problem, and it comes with important limitations and questions. There are concerns about energy consumption, scalability, regulation, and usability for everyday people. However, the ongoing innovation across public and private blockchains, combined with growing enterprise adoption, suggests that blockchain will remain a key pillar of digital transformation. Understanding how it works, where it is useful, and what challenges still exist is essential for businesses, developers, policymakers, and anyone interested in the future of the digital economy.

What Is Blockchain Technology?

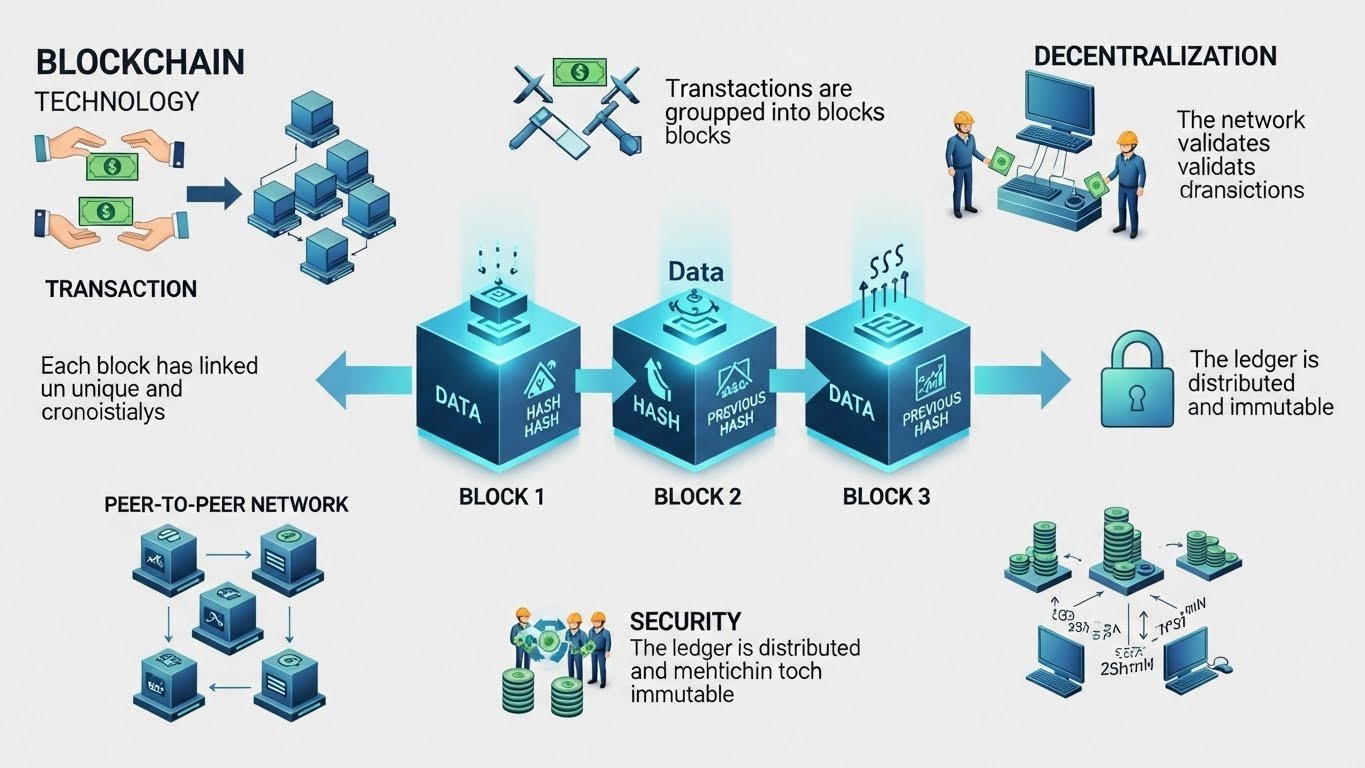

Blockchain technology is a type of distributed ledger system that records transactions in a secure, transparent, and tamper-resistant way. Instead of storing information in a single database controlled by one organization, a blockchain spreads the same information across many computers. Each participant in the network has a copy of the ledger, and all participants work together to verify and record new transactions. This architecture creates a shared source of truth that does not depend on a central authority.

In simple terms, a blockchain is a chain of blocks, and each block contains a list of transactions. When people talk about blockchain technology powering cryptocurrencies like Bitcoin or Ethereum, they are referring to this underlying network that maintains the record of who owns what. However, the concept goes far beyond digital currencies. Any type of digital record, from contracts to medical data to supply chain records, can be stored and tracked on a blockchain.

A key aspect of blockchain technology is immutability. Once information has been added to the chain and confirmed by the network, it becomes extremely difficult to change. This is because each block contains a cryptographic reference to the previous block, forming a linked chain. Altering any data would require recalculating these cryptographic links and convincing the majority of the network to accept the change, which is computationally expensive and practically infeasible in well-designed systems. This immutability is one of the reasons blockchain is seen as a powerful tool for auditability and transparency.

How Blockchain Technology Works

To understand how blockchain technology works in practice, it helps to look at the main components of a blockchain network. At the most basic level, there are nodes, transactions, blocks, and a consensus mechanism. Nodes are the computers that participate in the network and maintain copies of the ledger. Users submit transactions, such as sending digital tokens or triggering a smart contract, and these transactions are broadcast to the network of nodes.

Nodes group pending transactions into blocks. Before a block is added to the chain, the network must agree that the transactions inside it are valid. This is where the consensus mechanism comes in. Different blockchains use different consensus algorithms, such as Proof of Work or Proof of Stake, but they all serve the same purpose: to ensure that the majority of the network agrees on the state of the ledger without relying on a central authority. When a block is validated and accepted, it is linked to the previous block with a cryptographic hash, and the ledger is updated for all nodes.

Blockchain technology can be implemented as public, private, or consortium networks. In a public blockchain, such as Bitcoin or Ethereum, anyone can join the network, participate in the consensus process, and view the ledger. These networks are often used for open, permissionless applications that do not depend on a central gatekeeper. In private or permissioned blockchains, access is restricted to authorized participants, and a single organization or group of organizations controls who can validate transactions. These designs are often chosen by enterprises that need the benefits of distributed ledgers while still maintaining regulatory and governance requirements.

The security of blockchain technology relies heavily on cryptography. Every participant has cryptographic keys that allow them to sign transactions and prove ownership of digital assets without revealing their private keys. The combination of cryptographic signatures, consensus mechanisms, and decentralized data storage makes blockchain technology resistant to many of the attacks that threaten traditional centralized databases.

Smart Contracts and Decentralized Applications

One of the most important innovations built on top of blockchain technology is the concept of smart contracts. A smart contract is a piece of code stored on the blockchain that automatically executes when certain conditions are met. Instead of relying on a human intermediary to enforce a contract, the blockchain network itself enforces the rules defined in the code. This can dramatically reduce the need for manual verification, paperwork, and third-party oversight.

Smart contracts are the foundation of decentralized applications, often called dApps. These applications run on blockchain networks and are not controlled by a single company or central server. Developers can create decentralized finance platforms, gaming ecosystems, digital marketplaces, and more, all powered by smart contracts and secured by the underlying blockchain. Users interact with these applications using digital wallets that connect to the blockchain, allowing them to sign transactions and manage their digital assets.

Blockchain technology makes smart contracts particularly powerful because they inherit the security, transparency, and immutability of the underlying ledger. Once deployed, a smart contract’s code is publicly visible and difficult to change, which can increase trust among users. However, this also means that any bugs or vulnerabilities in the contract can be hard to fix after deployment, highlighting the need for careful design, testing, and auditing.

Key Use Cases of Blockchain Technology

While cryptocurrencies remain the most famous use case of blockchain technology, the potential applications extend across many industries. In finance and payments, blockchain enables faster, cheaper cross-border transactions, peer-to-peer transfers, and programmable money through tokens and stablecoins. Traditional payment rails often involve multiple intermediaries and settlement delays. By contrast, blockchain-based networks can process transactions around the clock, often with reduced fees and near-instant settlement.

Supply chain management is another major area where blockchain technology is making an impact. Complex supply chains involve many participants, from manufacturers and logistics providers to wholesalers and retailers. Tracking the origin, movement, and condition of products can be challenging with fragmented systems. Blockchain offers an immutable record of each step in the journey, enabling companies and consumers to verify authenticity, track provenance, and improve transparency. This is particularly valuable for high-value goods, pharmaceuticals, food safety, and sustainability reporting.

Identity and data management are also promising domains for blockchain technology. Today, personal data is scattered across countless platforms and databases, often controlled by large organizations. Blockchain-based identity solutions aim to give individuals more control over their digital identity and credentials. Instead of sharing copies of personal data with each service provider, users can store verifiable credentials in a wallet and selectively share only what is necessary. This concept, sometimes called self-sovereign identity, uses blockchain as a trust layer to verify the authenticity of credentials without exposing the underlying sensitive data.

In the realm of digital assets, blockchain technology enables tokenization, where real-world or digital items are represented as tokens on a blockchain. These tokens can represent everything from art and collectibles to shares in a company or fractions of real estate. Non-fungible tokens, or NFTs, are unique digital tokens that prove ownership of specific assets. Although the NFT market has been volatile, the underlying idea of programmable, verifiable ownership continues to inspire new business models in gaming, entertainment, and intellectual property.

Benefits of Blockchain Technology

The benefits of blockchain technology are closely tied to its core properties: decentralization, transparency, security, and immutability. By removing the need for a central authority, blockchain can reduce the risk of single points of failure. If one node in the network goes offline or is compromised, the rest of the network still holds the complete record. This resilience is particularly important for critical infrastructure and financial systems.

Transparency is another major advantage. Because transactions on public blockchains are visible to all participants, it becomes easier to audit and verify activity. This does not mean that personal information is exposed; blockchains generally use pseudonymous addresses rather than real names. However, the structure of the ledger allows regulators, auditors, and users to trace flows of value and detect suspicious behavior more easily than in opaque systems.

Blockchain technology also enhances security through cryptography and consensus. Transactions must be signed with a private key, and the network must agree on the validity of each block. Attacking a well-designed blockchain requires controlling a large portion of the network’s computing power or stake, which is extremely costly. While no system is perfectly secure, the decentralized architecture of blockchain makes many traditional attack vectors less effective.

Immutability supports trust and accountability. Once data is recorded on a blockchain and secured by consensus, it is resistant to tampering. This can be invaluable for record keeping in areas such as land registries, intellectual property, and compliance reporting. Organizations can use blockchain as a single source of truth that multiple parties can rely on without having to fully trust each other or maintain separate, redundant databases.

Limitations and Challenges of Blockchain Technology

Despite its advantages, blockchain technology faces several significant limitations and challenges that must be considered. One of the most frequently discussed issues is scalability. Many early public blockchains struggle to handle large volumes of transactions at high speed, leading to congestion and high fees during periods of heavy activity. Various scaling solutions, such as layer-two networks and alternative consensus algorithms, are being developed to address this, but no single approach has solved the problem for every use case.

Another concern is energy consumption. Some blockchain networks that use Proof of Work require substantial computational power, which translates into high electricity usage. This has raised environmental questions, especially as networks grow in popularity. Newer blockchains and upgrades to existing ones are adopting more energy-efficient mechanisms like Proof of Stake, which significantly reduce energy consumption while maintaining security, but the transition is still ongoing in some ecosystems.

Regulation and legal uncertainty also present challenges for blockchain technology. Governments around the world are still developing frameworks for cryptocurrencies, digital assets, and decentralized applications. Questions about compliance, taxation, consumer protection, and anti-money laundering obligations are complex and not fully settled. Businesses exploring blockchain solutions must navigate this evolving landscape carefully to avoid legal risks.

Usability is another barrier to mass adoption. For many everyday users, interacting directly with blockchain networks, managing private keys, and understanding transaction fees can be confusing and intimidating. Poor user experience can lead to mistakes, such as lost funds due to mismanaged keys. The next phase of growth for blockchain technology will require more intuitive interfaces, better education, and services that hide the technical complexity behind familiar experiences.

Blockchain Technology in Different Industries

The impact of blockchain technology can be seen across a growing number of industries. In banking and finance, institutions are experimenting with blockchain-based settlement systems, tokenized assets, and central bank digital currencies. These initiatives aim to increase efficiency, reduce counterparty risk, and enable faster, more inclusive payment systems. Some stock exchanges and clearing houses are exploring distributed ledger technology to modernize trade settlement processes and improve transparency.

In healthcare, blockchain technology is being tested for secure sharing of medical records, tracking of pharmaceuticals, and management of clinical trial data. Healthcare data must be accurate, confidential, and accessible to authorized parties. A blockchain-based system can create an audit trail of who accessed or modified records while helping prevent counterfeit drugs from entering the supply chain. This combination of traceability and privacy is particularly valuable in complex medical ecosystems.

Governments and public sector organizations are also exploring blockchain applications. Use cases include digital identity systems, land registration, voting systems, and public procurement. By leveraging blockchain technology, public services can potentially become more transparent, efficient, and resistant to corruption. For example, recording land titles on a blockchain can reduce disputes, fraud, and bureaucratic delays by providing a clear and tamper-resistant history of ownership.

Industries such as energy, logistics, and entertainment are using blockchain to support peer-to-peer energy trading, real-time tracking of shipments, and decentralized content distribution. In each case, blockchain technology acts as a shared ledger that multiple stakeholders can trust, reducing the need for intermediaries and improving coordination. While many of these projects are still in pilot stages, they illustrate the broad versatility of blockchain as a foundational technology.

The Future of Blockchain Technology

Looking ahead, the future of blockchain technology is likely to be shaped by increased integration with other emerging technologies. As artificial intelligence, the Internet of Things, and edge computing continue to grow, blockchain can serve as a secure backbone for exchanging data, automating processes, and managing digital identities. For example, IoT devices could use blockchain to record sensor data, trigger smart contracts, and settle micro-transactions without human intervention.

Interoperability will be a critical theme in the next wave of blockchain development. Today, many blockchains operate as separate ecosystems, which can limit the free flow of assets and data. Cross-chain bridges, interoperability protocols, and standards are being developed to connect these islands into a more unified network of networks. As this happens, users and businesses may no longer need to think about which blockchain they are using, similar to how most people do not worry about the underlying infrastructure of the internet today.

Regulatory clarity will also influence how widely blockchain technology is adopted. As policymakers gain a better understanding of decentralized systems and digital assets, more comprehensive frameworks are emerging. Clearer rules can encourage institutional participation, unlock new use cases, and protect consumers without stifling innovation. Many observers expect a gradual alignment between the benefits of blockchain technology and the requirements of global financial and legal systems.

For businesses, the future of blockchain technology is both an opportunity and a responsibility. Organizations that invest in learning, experimentation, and collaboration can discover new ways to improve efficiency, create value, and build trust with customers. At the same time, they must carefully assess which problems truly require a blockchain-based solution, rather than adopting the technology simply because it is a trend. Thoughtful design, strong governance, and alignment with real-world needs will determine which blockchain projects succeed in the long term.

Should You Care About Blockchain Technology?

Whether you are an individual, a business leader, or a policymaker, understanding blockchain technology is increasingly important. Even if you never buy a cryptocurrency or build a decentralized application, the principles behind blockchain are influencing how digital systems are designed. Concepts like decentralized trust, programmable money, tokenization, and self-sovereign identity are changing expectations about how data and value should be handled in the digital world.

For individuals, blockchain technology can offer new ways to save, invest, and participate in digital communities. It can also raise new responsibilities, especially when it comes to managing private keys and understanding risk. For businesses, the question is less about whether blockchain matters and more about where it can add meaningful value. This might involve streamlining supply chains, simplifying compliance, enhancing data sharing with partners, or creating new digital products and services.

Ultimately, blockchain technology is part of a broader shift toward more open, transparent, and programmable infrastructure. By learning how it works and where it fits, you can make better decisions about when to adopt it, how to regulate it, and what opportunities it may unlock in your industry or life.

FAQS

Q: What is the main purpose of blockchain technology?